Veda Financial | December 2025

Every year around this time, I get a similar phone call: “Year-end is here… and I need to reduce my taxable income by a lot. What can we do?”

Recently, a business owner reached out in exactly this situation. His company had a very strong year, and he suddenly realized he needed roughly $500,000 in deductions.

The solution was a coordinated retirement strategy using a Safe Harbor 401(k), a Profit Sharing plan, and a Defined Benefit pension plan. When used together, these plans can create remarkably high tax-deductible contributions, especially for owners and highly compensated employees. The Defined Benefit plan was the real driver — these plans allow much larger contributions because they’re designed to fund a future pension benefit. With the right design, they can be structured so that a meaningful proportion of the contributions goes to the owner while still meeting compliance rules.

Whether or not you need a six-figure deduction, year-end is a great time to take stock of the tools available. Here are strategies for business owners, entrepreneurs, employees, and anyone with retirement accounts.

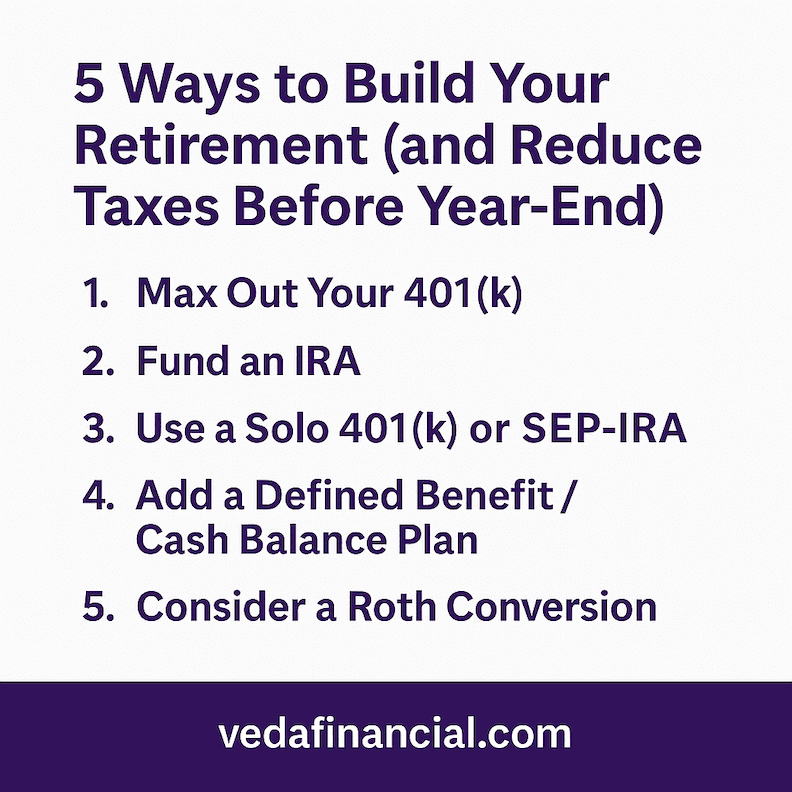

1. Maximize 401(k) Contributions (Employees and Employers)

If you have access to a 401(k) at work — or run your own company — this is a good place to start.

• Employees can contribute up to $23,000 in 2025, plus $7,500 if age 50+.

• Employer contributions (match or profit-sharing) can bring the total to $69,000+.

Example: Someone earning $180,000 who increases their contribution from a small percentage to the maximum can reduce taxable income significantly while strengthening retirement savings.

2. Open and Fund an IRA (Individuals and Spouses)

Even without a company plan, you can still create deductions through IRAs if your income allows.

• Contribution limit for 2025 is $7,000 per person (+$1,000 if 50+).

Example: A couple not covered by workplace plans may deduct up to $14,000 by fully funding two IRAs.

3. Solo 401(k) or SEP-IRA (Entrepreneurs & Freelancers)

If you’re self-employed with no full-time employees, these plans are powerful and flexible.

• A Solo 401(k) allows both “employee” and “employer” contributions — useful if you want to maximize deferral.

• A SEP-IRA allows up to 25% of net earnings, capped at $69,000.

Example: A consultant earning $250,000 might contribute $50,000+ into a SEP with minimal administration.

4. Defined Benefit Plans (High-Income Business Owners)

For those with steady income and a desire for large deductions, a Defined Benefit (or Cash Balance) plan is often the most impactful option.

• Contributions can reach well into the six figures depending on age and compensation.

• These plans can be layered on top of an existing 401(k).

Example: A 55-year-old owner might be able to contribute $200,000–$400,000+ per year with a properly designed plan.

5. Year-End Roth Conversions (Anyone With an IRA)

A Roth conversion doesn’t reduce taxes today — but it can secure tax-free growth forever. It’s especially valuable in down markets or low-income years.

Example: Someone temporarily in a lower tax bracket may convert part of their IRA now and permanently lock in a favorable tax rate.

THE BOTTOM LINE

Whether you need a large deduction or just want to optimize your tax picture before year-end, the right retirement and tax strategies can make a meaningful difference.